Let’s be honest.

Most companies today talk about sustainability because they have to — not because they fully understand it.

Words like net zero, ESG, carbon footprint, and BRSR show up in annual reports, presentations, and investor decks. But ask a simple operational question:

“What exactly is our environmental cost?”

And the room often goes silent.

This is precisely where environmental costing enters the picture.

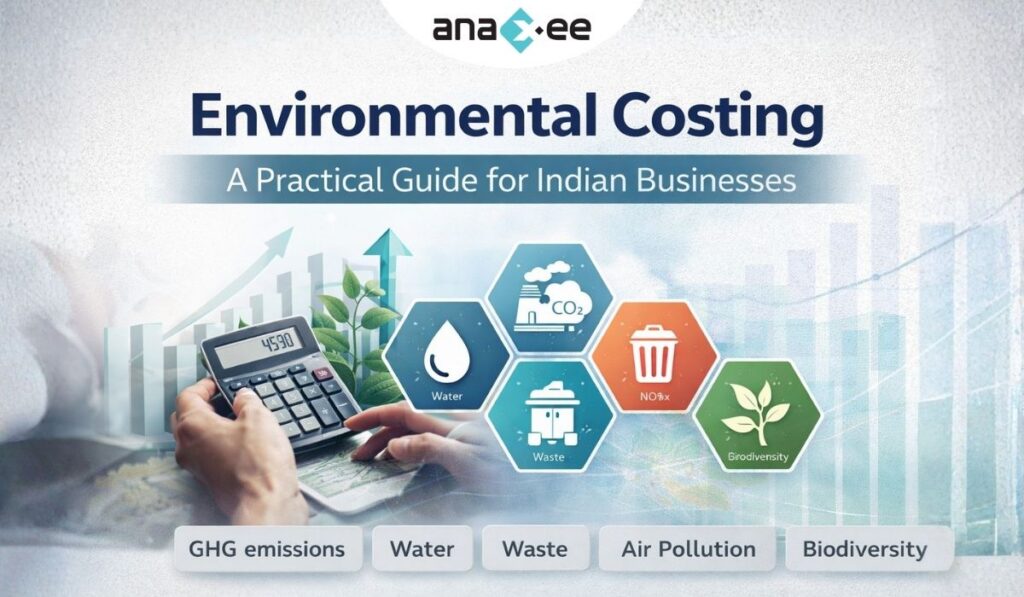

So, What is Environmental Costing?

In simple language:

Environmental costing is the process of measuring how much your business activities “cost” the environment.

Not in rupees.

Not in dollars.

But in physical impact units.

Think:

- Tonnes of CO₂ equivalent (GHGs)

- Litres of water consumed

- Tonnes of waste generated

- Units of air pollutants (NOx, SOx, PM)

- Impact on biodiversity

The Guidance Note on Environmental Costing by ICMAI frames this beautifully by highlighting one key idea:

Every business activity has a financial cost — and an environmental cost. R_GuidanceEnvironmentalCosting

We’ve spent decades perfecting financial bookkeeping. Environmental bookkeeping is now catching up.

Environmental Impact vs Environmental Cost

These terms are often mixed up.

Environmental Impact → What effect do your operations have

Environmental Cost → That impact is quantified and recorded

For example:

| Activity | Impact | Environmental Cost |

|---|---|---|

| Diesel usage | GHG emissions | kgCO₂e |

| Factory cooling | Water use | Litres |

| Packaging | Plastic waste | Tonnes |

| Chimney output | NOx/SOx | Absolute units |

Environmental costing turns vague statements into measurable numbers.

Why This Suddenly Matters

Because pressure is no longer optional.

Businesses are now being pushed by:

- Regulators

- Investors

- Customers

- Supply chain partners

In India, SEBI’s BRSR mandate requires environmental disclosures from top listed companies. And increasingly, value chain partners are being pulled into Scope 3 reporting.

Translation?

Even if you’re not listed, you’re not insulated.

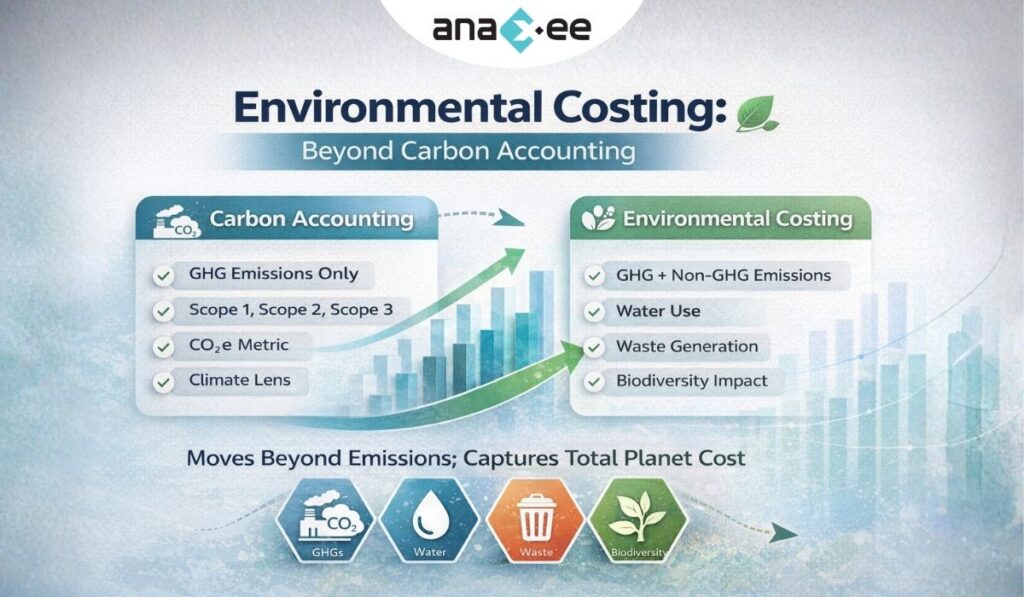

Beyond Carbon Accounting

Here’s a common mistake:

Many companies think sustainability = carbon footprint.

But environmental costing is multi-dimensional:

1️⃣ GHG Emissions

2️⃣ Non-GHG Emissions

3️⃣ Water

4️⃣ Waste

5️⃣ Biodiversity

Carbon is just one slice of the pie.

Ignoring the rest creates blind spots:

- Water-intensive operations

- Hidden waste leakage

- Air pollution liabilities

- Ecological risks

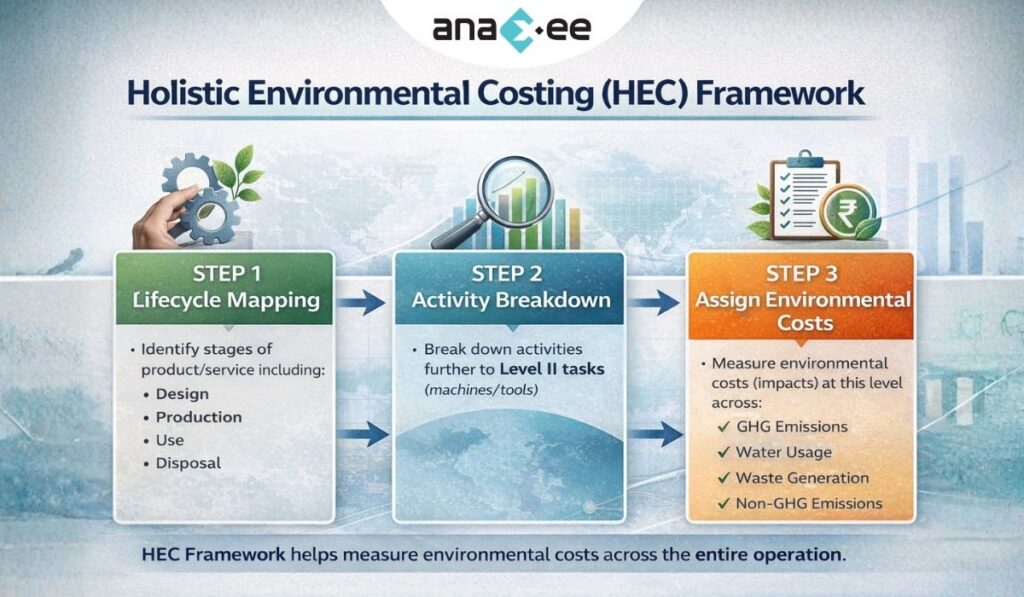

Enter the HEC Framework

ICMAI proposes the Holistic Environmental Costing (HEC) Framework R_GuidanceEnvironmentalCosting.

Instead of random data collection, HEC applies structured thinking:

Step 1 → Lifecycle Mapping

Step 2 → Activity Breakdown

Step 3 → Assign Environmental Costs

This mirrors traditional cost accounting logic — but applied to environmental impacts.

Lifecycle Thinking Changes Everything

Most companies measure what happens inside their walls.

HEC asks:

- What about design decisions?

- Supplier emissions?

- Product usage impact?

- End-of-life disposal?

Example:

An automobile manufacturer may not emit during driving — but the product certainly does.

Who owns that impact?

Technically → Customer

Practically → Shared responsibility

Environmental Costing is Also a Risk Tool

This isn’t just reporting compliance.

Environmental costing helps identify:

✔ Inefficiencies

✔ Resource leakages

✔ Regulatory exposure

✔ Climate vulnerabilities

If lubricant purchase ≠ lubricant consumption → something’s wrong.

If water use intensity rising → operational risk.

If waste generation inconsistent → process instability.

What Happens Without Environmental Costing

You get:

❌ Patchy ESG data

❌ Greenwashing accusations

❌ Poor investor confidence

❌ Weak sustainability strategy

❌ Surprise compliance shocks

And worse:

Decisions based on assumptions, not evidence.

Final Thought

Environmental costing is not a “CSR exercise.”

It is management intelligence.

Just like financial costing helps you understand profitability, environmental costing helps you understand sustainability performance and risk.

Companies that adopt this early gain:

- Better reporting credibility

- Stronger ESG positioning

- Clear mitigation pathways

- Competitive advantage

Because eventually:

Those who cannot measure impact will struggle to justify growth.