Why Most Non-FMCG Brands Overestimate Their Retail Reach in India

Walk into almost any kirana shop in India and you’ll find Parle-G.

From a village in Bihar to a crowded market in Mumbai, chances are the product is sitting somewhere on a shelf.

Now try naming an electronics brand, an automotive battery brand, a tyre brand, or a kitchen appliance company that can say the same.

You probably can’t.

Of course, non-FMCG products are different.

Nobody impulse-buys a car battery while buying snacks. A mixer grinder doesn’t belong next to a packet of biscuits. A tyre isn’t sold from a roadside grocery store.

That’s not the point.

The real question is:

Within the shops that should be stocking your products, how visible are you really?

For most non-FMCG brands, the answer is uncomfortable.

Not nearly as much as they think.

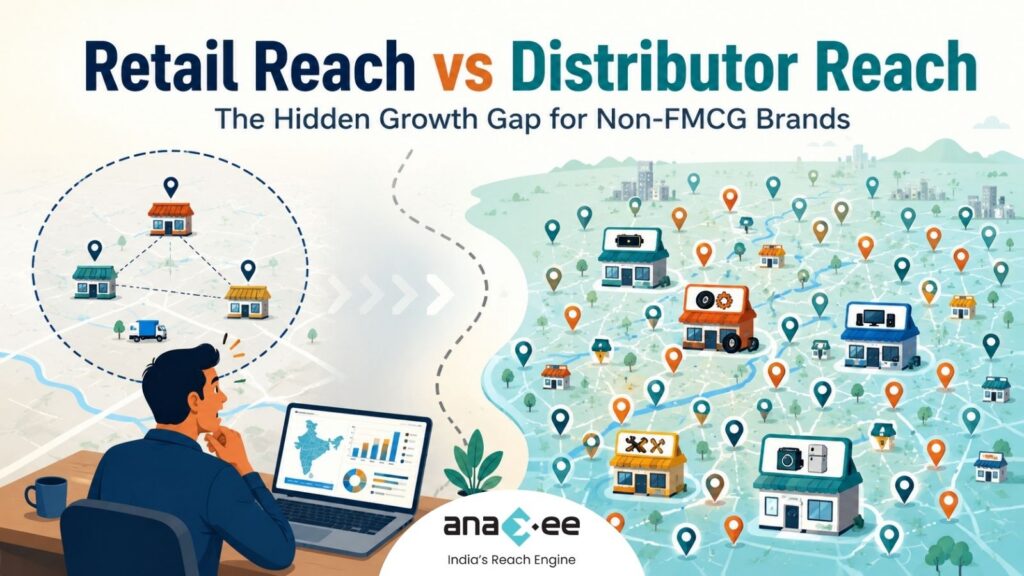

The Difference Between Distributor Reach and Retail Reach

Many brands assume that because they have appointed distributors across multiple districts, states, or regions, they have achieved market coverage.

What they actually have is distributor coverage.

Those are not the same thing.

Distributor reach is limited by factors such as:

- Existing retailer relationships

- Credit preferences

- Sales team capacity

- Route efficiency

- Distance from warehouse locations

- Local market familiarity

Over time, a company’s retail footprint starts looking less like a market opportunity map and more like a distributor comfort zone map.

The brand believes it has covered the market.

The market tells a different story.

The Visibility Problem Most Brands Never Measure

Ask a sales leader:

“How many retailers sell your product in District X?”

Most can answer.

Now ask:

“How many retailers could potentially sell your product in District X?”

The answer is usually far less clear.

And that’s where the problem begins.

You cannot measure market penetration if you don’t know the size of the market.

Without a complete retailer universe, brands often evaluate performance using incomplete information.

They compare sales against existing retailers instead of comparing sales against total market opportunity.

The result?

Large growth opportunities remain invisible.

A Real Example from Uttar Pradesh

To understand the scale of the problem, consider a recent retail mapping exercise.

Across just five districts in Uttar Pradesh, we identified more than 3,000 retail outlets selling kitchen appliances and utensils.

One category.

Five districts.

3,026 outlets.

The surprising part wasn’t the number.

The surprising part was how many of those outlets were missing from existing market visibility systems.

Many brands assume they have strong market coverage because sales are coming in.

But sales coming in does not automatically mean market coverage is high.

There can still be hundreds or thousands of relevant retailers that have never been approached, mapped, or activated.

India’s Biggest Growth Markets Are Still Offline

One reason this gap exists is because India’s growth story is often misunderstood.

Most business conversations focus on metros.

But retail reality looks very different.

Consider these facts:

- Approximately 88% of Indians live outside major metropolitan cities

- Around 70% of household consumption happens outside metros

- A significant share of non-FMCG commerce still happens through offline retail channels

For categories such as:

- Automotive batteries

- Tyres

- Lubricants

- Electrical goods

- Consumer durables

- Kitchen appliances

- Hardware products

The local retailer remains the primary point of purchase.

The challenge is that many of these markets are fragmented, dispersed, and difficult to track.

They are not small markets.

They are simply harder to reach.

Why Distributor-Led Expansion Has Limits

Distributors play a critical role in growth.

No serious brand can scale without them.

But distributors face practical constraints.

Every distributor prioritizes:

- Profitable routes

- Existing relationships

- Creditworthy retailers

- Efficient delivery schedules

This is understandable.

However, it means many potentially valuable retailers remain outside the network.

Not because they don’t matter.

But because they are harder to serve.

Over time, brands unknowingly inherit these limitations.

As a result, expansion slows down long before market opportunity is exhausted.

The Missing Layer: Retail Intelligence

The solution is not replacing distributors.

The solution is giving them better visibility.

Before a market can be activated, it must be understood.

Brands need answers to questions such as:

- Which retailers exist in a market?

- What categories do they sell?

- Which brands are already present?

- Which retailers are active?

- Which retailers have growth potential?

- Where are the white spaces?

This is where retail intelligence becomes important.

Instead of operating with assumptions, companies begin operating with facts.

Retail Mapping Creates New Growth Opportunities

When brands build a verified retailer database, several things happen.

First, they identify previously unknown outlets.

Second, they uncover underserved territories.

Third, distributors gain access to new prospects.

Fourth, sales teams can prioritize high-potential markets.

The result is not just better visibility.

It is better execution.

And better execution eventually becomes growth.

From Market Assumptions to Market Reality

Many non-FMCG brands have spent years investing in distribution.

The next phase of growth will come from investing in visibility.

Because you cannot expand into markets you cannot see.

You cannot activate retailers you do not know exist.

And you cannot measure penetration without understanding the total opportunity.

The brands that win over the next decade will not necessarily have the biggest distributor networks.

They will have the clearest picture of the market.

Final Thought

The goal is not to become the next Parle-G.

The goal is to maximize presence within the retail universe that matters for your category.

For automotive brands, that means being visible across relevant auto parts stores and workshops.

For appliance companies, that means reaching more dealers and retailers.

For electronics brands, it means identifying and activating the right outlets before competitors do.

Growth is rarely hiding in places nobody knows about.

More often, it is hiding in places nobody has mapped.

And until you know where those retailers are, your market coverage is probably smaller than you think.

About Anaxee

Anaxee Digital Runners helps brands discover, map, verify, and activate retail networks across India. Through a combination of last-mile execution, retail intelligence, and technology-enabled workflows, Anaxee enables companies to gain visibility into markets that traditional distribution systems often miss.

Want to know how many relevant retailers actually exist in your target market?

Contact sales@anaxee.com to explore retail mapping, retailer verification, and market expansion. A complete GTM solution for your brand.